5 Inventory Analysis Methods for Better Stock Control

Inventory analysis is the process of determining the optimal inventory level for a company to avoid stockouts or overstocking. It is particularly important for wholesalers of durable goods, as market demand can fluctuate and vary greatly over time. Knowing your inventory, maintaining efficient processes for managing stock levels, and monitoring and responding to changes in customer demand are all essential for effective inventory management.

Managing inventory accurately is vital for wholesalers. There are many common challenges to navigate when optimising inventory levels. Inventory control can easily become unbalanced when warehouse locations have excess stock or obsolete stock, resulting in tighter budgets and less available working capital.

Inventory control and inventory optimisation are like walking a high wire blindfolded; without the right tools and processes, it’s going to go wrong. Without the right tools and processes for confident forecasting, profitability and growth will be at risk.

Choosing the right inventory analysis method helps distributors understand which products are driving revenue, which are tying up cash, and where stock levels need adjusting.

In this guide, we’ll explain five common inventory analysis methods and show when each is most useful for making smarter replenishment decisions. These inventory management methods are especially useful for inventory management teams that need to improve availability, reduce waste and excess inventory, and keep working capital under control.

Inventory analysis methods at a glance

Inventory analysis vs inventory control vs inventory valuation

Inventory analysis, inventory control, and inventory valuation are closely connected, but they are not quite the same.

- Inventory analysis is about understanding how stock performs, where demand is changing, and which items deserve the most attention.

- Inventory control is about the day-to-day processes used to manage stock levels, replenishment, and warehouse movement.

- Inventory valuation is the accounting method used to assign a value to stock, which affects cost of goods sold, profit reporting, and the balance sheet.

For distributors, the best results come from using all three together. Analysis shows what is happening, control helps you act on it, and valuation helps finance teams understand the true cost and value of the stock being held. Inventory valuation methods, such as FIFO, LIFO, and average cost, are also inventory costing methods because they influence the cost of goods sold and how inventory appears on the balance sheet.

3 costly inventory analysis mistakes made by distributors

We’re all human, and mistakes happen, but in supply chain management, even a small one can be costly. Below are three inventory analysis problems that wholesale distributors face, which can be extremely costly if not addressed:

- Not dealing with excess stock. Regular excess stock analysis helps distributors identify slow-moving items before they tie up too much working capital or become obsolete. Efficient inventory monitoring ensures that due priority is given to the more profitable, high-turnover inventory items and separates those that may be numerous but less profitable or slower-moving. Knowing your item-level inventory turnover ratio is vital when analysing stock health. For example, do you have enough of your A-classified goods in stock to meet supply, and do you need to keep a C-classified product in stock, or are they just tying up working capital? Additionally, not dealing with excess stock promptly can lead to inventory obsolescence, which can be even more costly to business operations.

- Poor handling of inventory obsolescence. Effective obsolete stock management means identifying at-risk items early, setting clear review criteria, and taking action before the inventory loses more value. All wholesale businesses face unpredictability, and there will be occasions where unwanted or obsolete stock is carried due to over-ordering or an unanticipated fall in demand. While this stock is unlikely to sell for a profit, it needs to be liquidated from inventory to avoid even larger financial losses for the company over time. Most items in a warehouse that have not sold within 12 months can be classified as obsolete and should be systematically removed from inventory to offset unnecessary carrying costs.

- Not analysing inventory seasonality. An important element of ensuring supply meets demand is understanding how customer behaviour for a product is affected by seasonal changes. This helps account for and prepare for periods of higher and lower demand, which may involve adjusting procurement rates at different times of the year or storing extra inventory to be on hand during peak seasons. For wholesale distributors, carefully managing safety stock levels is the best way to manage and account for demand volatility in the supply chain.

Common inventory analysis methods

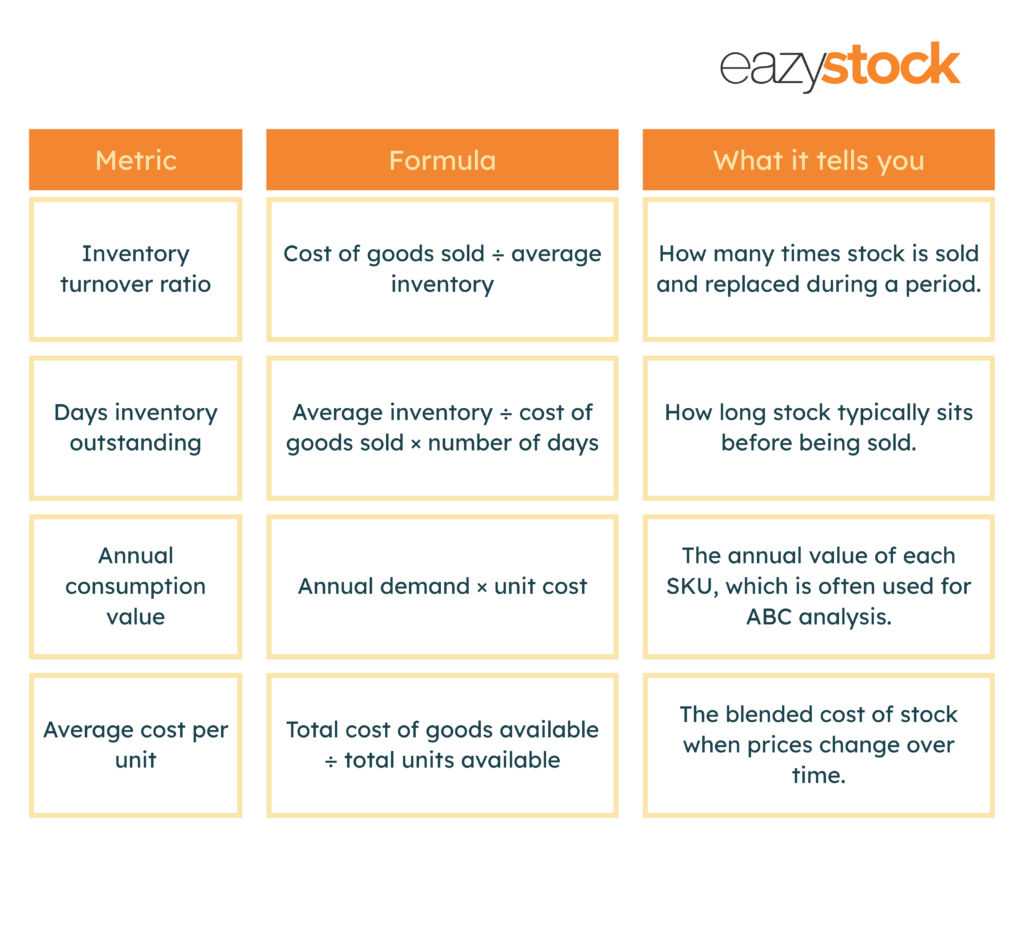

Inventory managers use several methods to analyse stock levels. Inventory analysis methods commonly involve either considering the overall inventory turnover (the cost of goods sold divided by the average inventory) or using the average daily cost of goods sold to determine the total number of days’ stock remaining in inventory.

Useful inventory analysis formulas and KPIs

Inventory analysis becomes much easier when everyone is working from the same numbers. These formulas are a useful starting point for reviewing stock health, identifying slow movers, and understanding how quickly inventory is being converted into sales.

These KPIs are useful on their own, but they are even more powerful when combined with demand forecasts, supplier lead times, seasonality, and service level targets. Holding less inventory may look efficient on paper, but if it increases stockouts, lost sales, or emergency purchasing, it does not actually improve inventory performance.

Different inventory analysis methods, techniques, and best practices include:

ABC analysis is a method for categorising stock by its value to the business. In inventory management, ABC analysis helps teams focus time, budget, and planning effort on the SKUs that matter most, with the most valuable items assigned to A (‘the critical few’), and the least valuable to C (‘the trivial many’). A, B, and C classifications are assigned to items with high, medium, and low annual consumption value, respectively. Placing class A items closer to your warehouse’s shipping and receiving area will save time and labour costs when processing customer orders. Inventory optimisation software is commonly used to identify which items should be classified into which category.

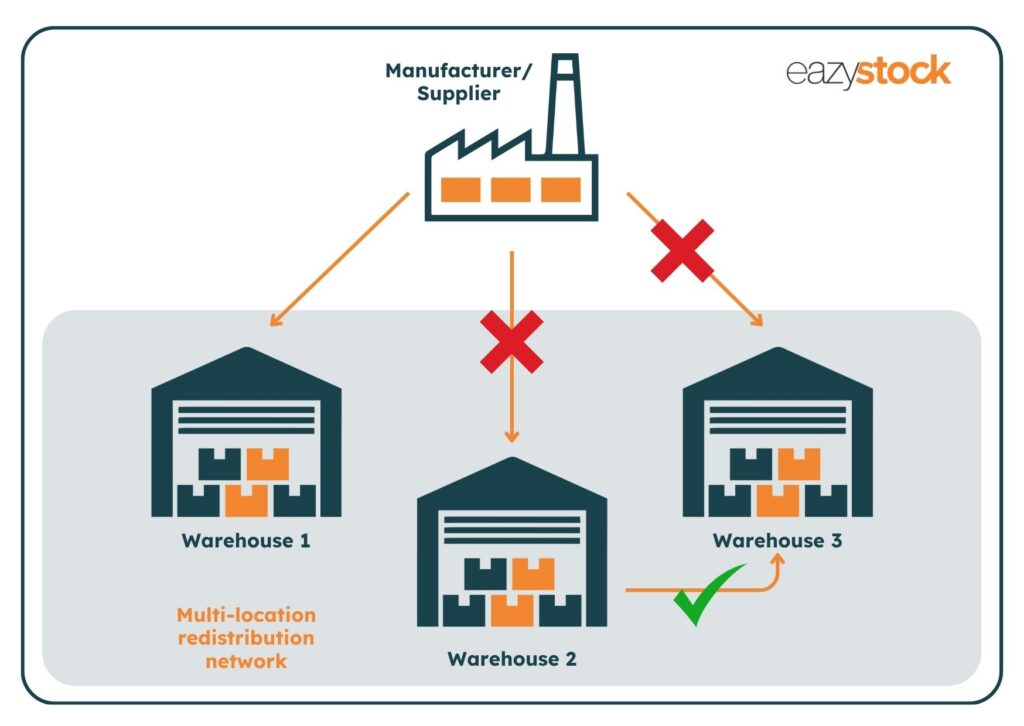

Inventory redistribution is the process of automatically transferring items between stocking locations, such as different warehouses, where demand for certain items may be higher in different regions. Redistribution is critical for businesses looking to avoid purchasing additional stock of items already heavily stocked within the company’s network of storage locations. This method is ideal for fast-moving industries or those with high seasonality, as items are less dependent on supplier lead times. As illustrated in the example below, a wholesale distributor with multiple warehouse locations can redistribute excess stock from Warehouse 2 to Warehouse 3 at a fraction of the cost of purchasing new stock from the manufacturer or supplier. Demand is still met, and additional working-capital costs are avoided.

- First In, First Out (FIFO) is the method in which the oldest inventory items are sold first, and the newest products are sold last. The FIFO inventory method is useful when older stock needs to move first, especially for items with expiration dates, shelf-life limits, or a higher risk of obsolescence. When an item is sold, the oldest cost associated with that item is removed from inventory. That cost is then reported on the income statement as part of the cost of goods sold. FIFO also means that the more recent costs of an item will remain in the inventory account and be reported on the balance sheet. This is the most common method used by distributors today for items with expiration dates.

- Last In, First Out (LIFO) is when the most recently produced items are sold first. The LIFO inventory method can be used in some accounting environments where costs are rising, and reporting standards allow it. LIFO is a popular accounting inventory management method for manufacturers or distributors that deal with frequent fluctuations in the cost of items purchased. In this case, the more expensive items are used first. The use of LIFO will result in less taxable income and lower income tax payments than the FIFO method if the cost of goods sold increases over time. Over a long period, or when costs increase dramatically, the lower income tax payments will be significant.

Average cost is less commonly used because it treats older and newer stock the same and simply takes the mean cost of all stock, regardless of its current market value. The average cost inventory method creates a blended cost across older and newer stock, which can be helpful when purchase prices fluctuate regularly. However, this method can be less reliable for accurately reporting the cost of goods sold and inventory values on the balance sheet.

Which method is the best for wholesale distributors?

For wholesale distributors of durable goods, if the cost of materials or finished goods from suppliers tends to increase over time (what doesn’t?), using LIFO will typically result in lower taxable income than using the FIFO method.

Distributors should keep in mind that to maintain a relatively strong balance sheet, which helps a company qualify for loans, satisfy investor expectations, or impress industry analysts, the FIFO method may be the better option, as working capital tends to look stronger.

How to choose the right inventory analysis method

No single inventory analysis method works best for every distributor, SKU, or warehouse. The right approach depends on what you are trying to fix. If too much cash is tied up in slow-moving stock, start with ABC analysis to identify which items need the closest attention. If products are available in one warehouse but missing from another, consider redistributing inventory to improve availability without immediately buying more stock. Redistribution can also offset the need to procure larger quantities of items that risk obsolescence. Since most suppliers require larger-quantity bulk orders to secure volume price discounts, redistribution can be a far less expensive option.

If your products expire, deteriorate, or become obsolete quickly, FIFO is usually the safer operational approach because older stock is used first. If purchase costs fluctuate and you need a simple view of stock value, average cost may be easier to manage. LIFO can be useful in some accounting environments where costs are rising, but distributors should check which reporting standards apply before relying on it.

In practice, most wholesale distributors need a combination of methods. ABC analysis helps prioritise planning efforts; FIFO supports effective stock rotation; redistribution improves network-wide availability, and valuation methods help finance teams report inventory accurately.

For those simply looking for a blended average of costs, the Average Cost method is the easier option.

How inventory optimisation software improves inventory analysis

Manual inventory analysis can quickly become time-consuming, especially when managing thousands of SKUs across multiple branches, warehouses, or regions. Inventory optimisation software consolidates demand data, stock levels, supplier lead times, service levels, and item classifications in a single platform.

Instead of relying on static spreadsheets, inventory teams can use automated analysis to identify excess stock, flag items at risk of stockout, adjust safety stock levels, model seasonality, and recommend more accurate replenishment quantities. This makes inventory analysis more proactive, helping distributors act before stock problems lead to lost sales, write-offs, or unnecessary carrying costs. For distributor inventory management teams, this transforms inventory analysis from a backwards-looking reporting task into a daily decision-making tool to optimise stock.

Inventory analysis FAQs

Inventory analysis is the process of reviewing stock data to understand demand, availability, value, movement, and risk. It helps businesses decide what to buy, when to buy it, where to store it, and how much to buy to meet customer demand without overstocking.

Common inventory analysis methods include ABC analysis, FIFO, LIFO, average cost, and inventory redistribution. Each method examines inventory from a slightly different perspective, such as stock value, stock age, accounting cost, or warehouse location.

Inventory costing methods are used to calculate the cost of goods sold and the value of inventory still on hand. Common examples include FIFO, LIFO, and average cost, all of which affect the cost of goods sold, profit reporting, and inventory valuation.

ABC analysis categorizes inventory into A, B, and C groups based on value or importance. A items are typically the highest-value products and require closer monitoring, while C items are lower-value products that can often be managed with simpler rules.

FIFO stands for first in, first out, meaning the oldest inventory is sold first. LIFO stands for last in, first out, meaning the newest inventory is sold first. FIFO is often used for products that expire or become obsolete, while LIFO is primarily an accounting method used in specific reporting environments.

The best method depends on the distributor’s goals. ABC analysis helps prioritize high-value SKUs; redistribution balances stock across locations; FIFO improves stock rotation; and average cost simplifies valuation when purchase prices vary.

Inventory analysis should be reviewed regularly, not just once a year. Fast-moving or high-value items may require frequent checks, while slower-moving items can be reviewed less often. The key is to analyze stock often enough to spot shifts in demand, supplier delays, and excess inventory before they become costly problems.

Inventory optimization software supports stock optimization by using demand forecasts, supplier lead times, service targets, and stock rules to recommend improved replenishment decisions. This helps distributors reduce excess stock, avoid stockouts, and improve working capital.